Dow Jones Industrial Average on the defensive as hot PPI fuels Fed angst

- US Producer Price Index for April surged to 6% YoY, the biggest jump since December 2022 and well above the 4.9% consensus.

- Boston Fed President Susan Collins has aligned with FOMC dissenters and openly floated a rate hike scenario.

- Senate confirmation vote on Kevin Warsh as next Fed Chair scheduled for around 18:00 GMT, two days before Powell's chair term ends.

- President Trump landed in Beijing for the Xi summit, but markets are fading hopes for a breakthrough as the Iran war hands China more leverage.

Dow Jones Industrial Average (DJIA) futures slipped onto the back foot through European and early US hours on Wednesday, struggling to hold above 49,500 after fading from overnight highs near 49,800. The S&P 500 and Nasdaq Composite are also nursing losses, with risk sentiment souring on a blistering wholesale inflation print and a hawkish chorus from Federal Reserve (Fed) officials. Add in a high-profile Senate vote to install Kevin Warsh atop the Fed and President Trump's arrival in Beijing for a high-stakes summit, and traders have plenty of reasons to keep risk dialled down.

Hot PPI deepens the pipeline inflation story

The April Producer Price Index (PPI) jolted markets, with headline prices rising 1.4% MoM, nearly triple the 0.5% consensus and the largest monthly increase since March 2022. On a YoY basis, PPI accelerated to 6%, far above the 4.9% consensus and the hottest reading since December 2022. Core PPI, which strips out food and energy, climbed 1% MoM and 5.2% YoY, also smashing forecasts of 0.3% and 4.3% respectively. Energy did most of the heavy lifting, with gasoline prices surging 15.6% as the war with Iran continued to squeeze global Oil flows. But the services side also lit up, climbing 1.2% for the biggest gain since March 2022, a worrying signal that pipeline pressures are spreading well beyond fuel costs.

Collins puts a rate hike on the table in Boston speech

Fed officials have grown markedly more uncomfortable with the inflation backdrop, and Boston Fed President Susan Collins drove that point home in remarks to the Boston Economic Club on Wednesday. While stressing it is not her base case, Collins said she "could envision a scenario in which some policy tightening is needed to ensure that inflation returns durably to 2% in a timely manner". She also took a direct shot at the dovish playbook, noting that "more than five years of above-target inflation has reduced my patience for 'looking through' another supply shock", and warned the Iran war's hit to global supply chains will linger even if a deal is struck soon. Collins, a non-voting Federal Open Market Committee (FOMC) member this year, expects the current slightly restrictive stance to stay in place "for some time", with high inflation unlikely to abate until 2027. With Tuesday's hot Consumer Price Index (CPI) report and Wednesday's even hotter PPI release feeding into the picture, traders are taking the hike talk seriously, with futures pricing now showing roughly a 40% chance of a hike by year-end and effectively no probability of a cut in June.

Warsh Fed Chair vote teed up for 18:00 GMT

The political backdrop adds another layer to the Fed narrative. The Senate is scheduled to vote on Kevin Warsh's confirmation as Fed Chair at around 18:00 GMT, after Tuesday's 51-45 vote confirmed him to the Board of Governors. Warsh, a Fed governor between 2006 and 2011 and a known inflation hawk, has pitched what he calls "regime change" at the Fed, including a smaller balance sheet and tighter coordination with the Treasury. Markets are watching closely because Powell's term as chair expires Friday, and Powell has confirmed he intends to remain on the Board through January 2028 to defend the institution's independence. With CPI and PPI both sitting at three-year highs, Warsh's first FOMC meeting on June 16-17 looks set to be anything but quiet.

Trump-Xi summit hopes fade as Iran war hands China leverage

President Trump landed in Beijing on Wednesday, his first visit to China since 2017 and his second face-to-face with Xi Jinping in under a year after their October sit-down on the sidelines of the APEC summit in Busan. The two leaders are scheduled to meet Thursday and Friday with trade, Taiwan, artificial intelligence and the Iran war all on the agenda, but the optimism that usually accompanies such summits is conspicuously absent. The problem for the US side is timing. With the Strait of Hormuz still under a US blockade and Iran's foreign minister Abbas Araghchi having just visited Beijing, China is sitting on more leverage than at any point since the conflict began, not less. Trump has already described the current ceasefire as on "massive life support" and his aides are reportedly weighing a resumption of combat operations. Far from softening Xi's position, the US-Iran standoff is reinforcing the Chinese leader's home turf advantage, and equity traders are responding by dialling back expectations for any meaningful trade or geopolitical wins from the trip.

What's next

Attention now turns to Thursday's data dump at 12:30 GMT, with Initial Jobless Claims expected at 205K and April Retail Sales forecast to rise 0.5% MoM, alongside the closely watched Retail Sales Control Group. Any sign of consumer pullback would harden the stagflationary tone that has driven this week's defensive bid in stocks, while a resilient print could give the hike camp at the Fed even more ammunition. Friday's NY Empire State Manufacturing Index and Industrial Production round out the week, but the macro spotlight will remain firmly on Beijing and the Senate floor.

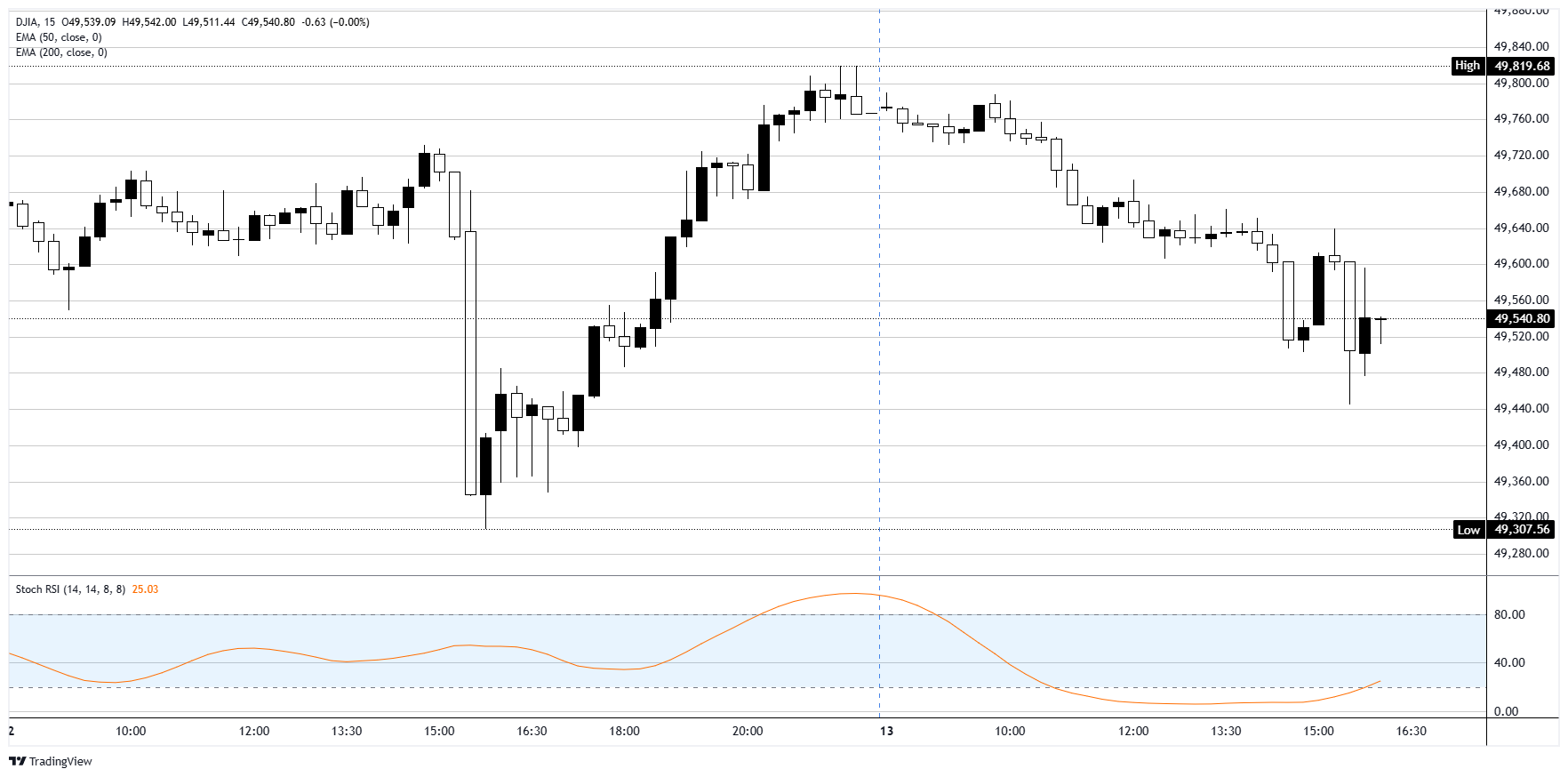

Dow Jones 15-minute chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.